Saving keeps your money safe; investing makes it grow. Grab any 401(k) match (free money), knock out high-interest debt, open a Roth IRA, and buy boring low-cost index funds — then automate it. The secret isn't picking winners. It's starting early and letting compound interest do the work over decades.

Saving and investing are not the same thing

Saving is keeping money safe. Investing is putting money to work. Your savings account is a responsible houseplant — it sits there and doesn't die, but it doesn't really grow either. Thanks to inflation (the quiet way prices creep up every year), money parked in a basic savings account slowly loses buying power.

Keep your emergency fund in savings — that part doesn't change. Investing is for money you won't need for a long time: your future self's money.

Meet compound interest, your lazy genius employee

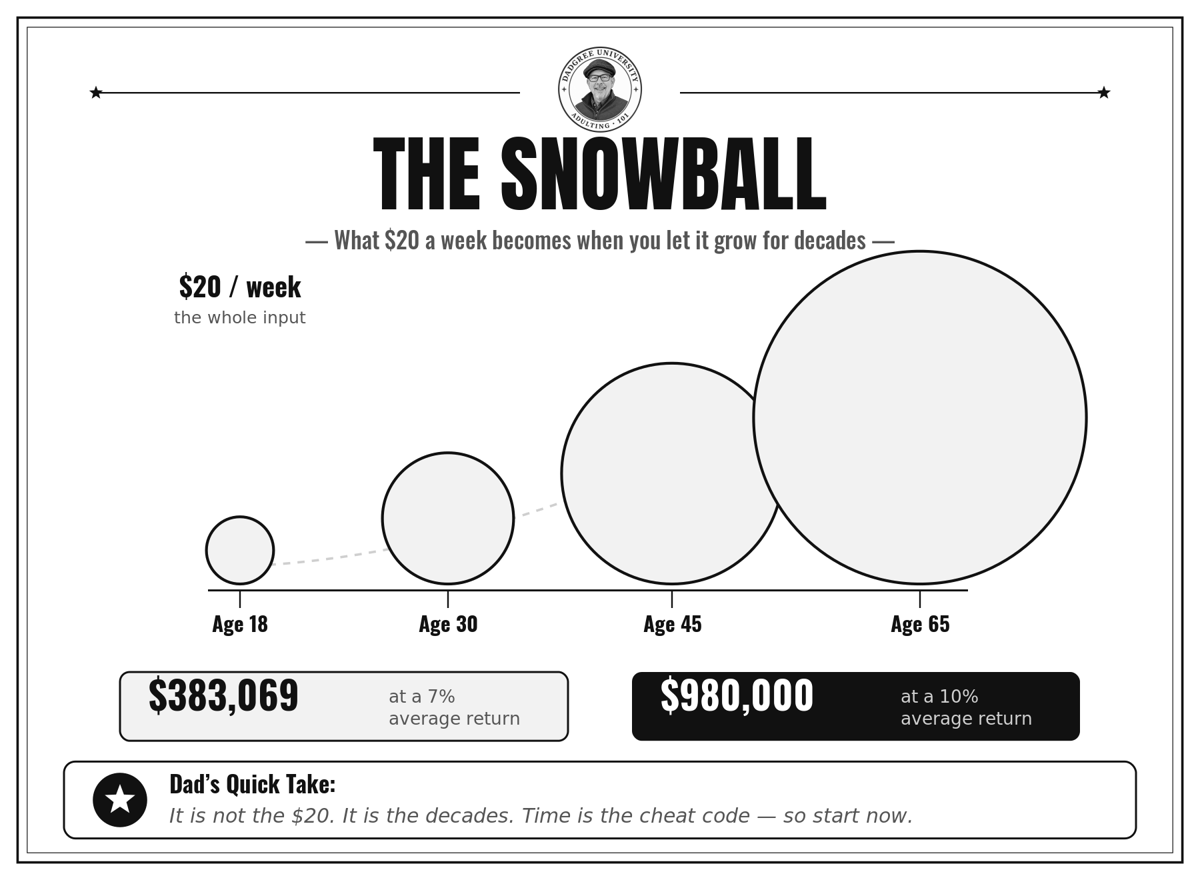

Compound interest is your money making money, and then that new money also making money. It's a snowball. It starts pathetic — grape-sized — and you'll be tempted to quit because nothing seems to be happening. Then you keep rolling it, and one day it's the size of a car, then a small building, and you did not get noticeably stronger. You just kept rolling.

That's why time is the real ingredient. The single most important sentence here: the best time to start was years ago; the second best time is today.

“But isn't this basically gambling?”

No. Day-trading meme stocks and throwing rent money at whatever coin a stranger is yelling about online — that's gambling. Boring, long-term investing in the whole market is closer to planting trees: you're not guessing which single tree grows fastest, you're buying a slice of the entire forest and letting it grow.

- “I don't have enough to invest.” You can start with very little. The habit matters more than the amount.

- “I'll lose it all.” Losing everything would take every major company on earth hitting zero at once — and then we'd all have bigger problems. But don't misread that: you can absolutely lose money, especially in the short run. Spread out, leave it alone for years, and time smooths the bumps. Never invest money you need next spring.

- “I'm not smart enough.” Good news: the smart move is the simple, boring one. The people who try to be clever usually do worse.

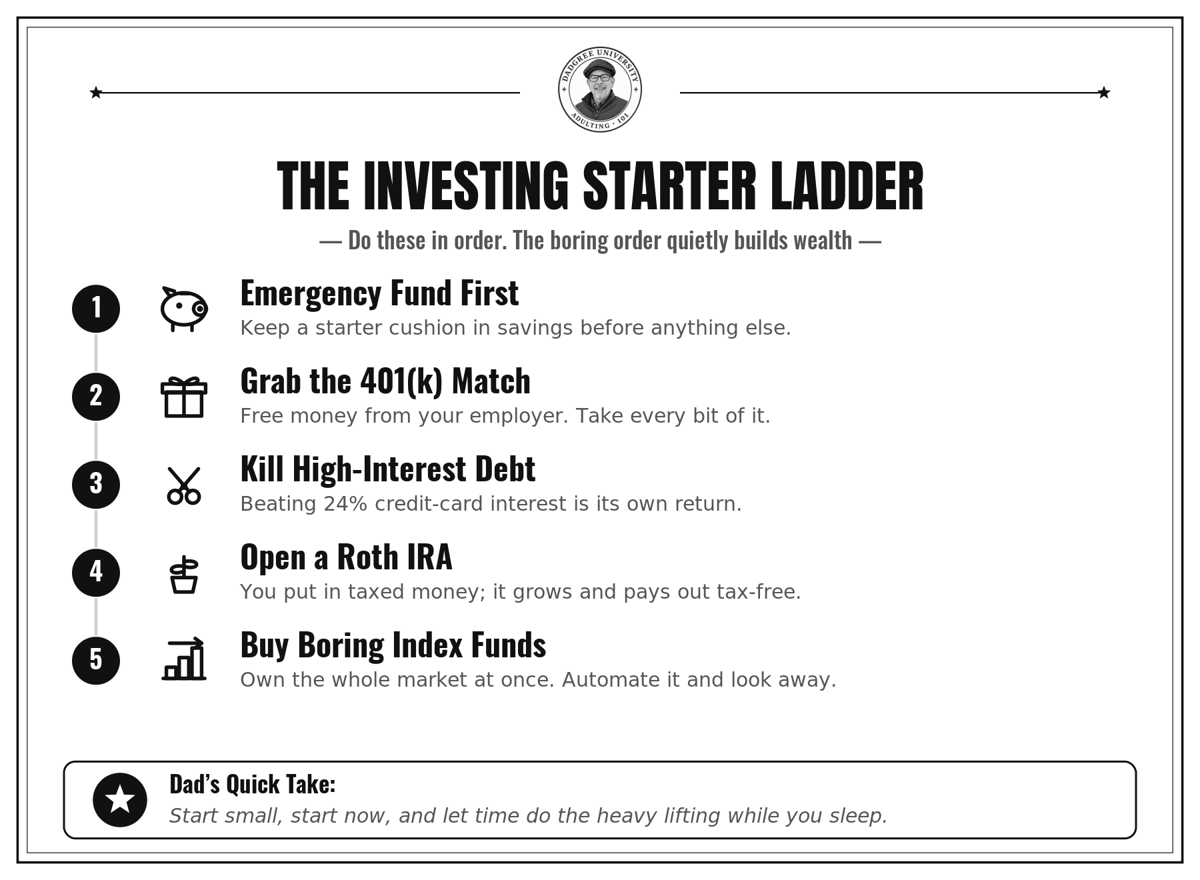

The boring starter ladder

Here's the order. Do them in order — don't skip to the exciting stuff before the boring stuff is handled.

- Emergency fund first. Keep a starter cushion in savings so future-you's money never becomes this month's rescue.

- Grab the 401(k) match. If your job matches contributions, contribute enough to get all of it — it's free money from your employer.

- Kill high-interest debt. Credit-card interest often grows faster than investments do. Beating a 24% goblin is its own kind of return.

- Open a Roth IRA. You put in money you've already paid taxes on; it grows and comes out in retirement tax-free. A very good deal when you're young.

- Buy boring index funds. Instead of betting on single companies, own a tiny piece of hundreds at once. Set up an automatic monthly contribution and look away.

Brokerage account: the account you use to buy investments. 401(k): a retirement account through your job, often with a match. Roth IRA: a retirement account you open yourself that grows and pays out tax-free. Index fund: one purchase spread across a whole pile of companies. Compound interest: money making money making money.

Keep it boring on purpose

The internet is full of people promising to make you rich fast. Almost all of them are selling something, lying, or about to learn an expensive lesson on camera. Real investing is slow, dull, and shockingly effective: start now, automate it, spread out, keep costs low, and — the hard part — don't panic and yank your money out the first time the market dips.

I'm a dad, not your financial advisor, and this is plain-English basics — not personalized advice. For your specific situation, talk to a qualified professional. But don't let “I should ask a pro someday” become the reason you never start.

Want the full, calm version with all the jokes? It's Chapter 3 of the Dadgree book.

Get your DadgreeCommon questions

How much do I need to start?

Often very little — many funds and apps let you start small. Consistency beats size every time.

Isn't investing risky?

Short-term, markets go up and down. Long-term and diversified (like index funds), they've historically grown. Invest money you won't need for years, and don't panic-sell.

Where do I actually open these?

A 401(k) is set up through your employer; a Roth IRA and index funds go through a reputable brokerage. Look for low fees and automatic contributions.